The solution that’s working for us may work for your company, too

Every business faces the challenge of managing health care costs. These costs will likely remain high even with Congress looking at changing the Affordable Care Act since they are talking about continuing child coverage to age 26 along with no pre-existing conditions. I thought I would share how we solved Health Care for our company—and why you may want to explore the option we took with your own company.

For those of you who don’t already know, my brother Daniel and I have combined ownership of Vincent’s Heating and Plumbing and Online-Access. Since retaining good employees is the battle we all face, we try to offer a good benefit package. We cover 70% of our employee’s healthcare premiums for their entire family. We offer a ‘Gold’ plan with a $1,250 deductible and then a 20% co-pay up to $5,000 ($1,000 per person). The total out of pocket amounts are doubled for a family plan.

In August of 2014, our company faced a combined premium increase that averaged about 37%. Our annual premium was going to be over $160,000 for 6 families, 3 couples, and 4 singles. And the craziest part was, that everything that we were reading was telling us that the premium hikes would not be the last we see under the Affordable Care Act (ACA)—which has proven absolutely true.

By going ‘outside the box’ and working with a self-insurance management company, we discovered that we could offer the same coverage for 14% less ($22,000 savings), with the potential to get reimbursed up to 40% of this lower premium at the end of the year, dependent on that year’s claim history. The company had had this program in operation for the last five years and, based on their previous three years of refunds to their participating companies, their average refund had been about 21%. We figured the projected refund at the end of the year for us would probably be about $35,000, for a combined savings of $57,000 from the premiums we would be paying by staying in the ACA insurance pool.

We went with the program and used the immediate savings to contribute monthly to a medical health savings plan for each family to cover 50% of what their out-of-pocket would be. Two months ago, we got our cash refund of the unused premium for the first year and it was actually 50% higher than we had projected. We don’t expect to see that type of refund every year, but the program was definitely a winner—and our premiums didn’t go up for 2016.

Our first reaction when we thought of self-insurance was to see it as a huge risk and potential liability. However, even though it is self-insurance, there is really little to no risk since the plan has a ‘Stop-Loss’’ policy from an A+ rated company that pays the claims completely for individual claims beyond $ 500/insured/year. Self-insurance is covered differently under the Affordable Care Act. However, it is not nearly as burdensome since only portions of the law apply. The ACA does tax self-insured plans, but again the tax is lower and not all taxes apply, further saving dollars on your premium.

Because the dollar savings are so substantial, looking at a managed self-insurance plan is definitely worth your while to understand how they work compared to typical plans using the ACA as the insured pool. Even without the immediate savings, it is worth it as the best long term option since everything points to the fact that everyone will continue to see premiums rise dramatically under the Affordable Care Act—which has not been the historical case for self-insurance. The program we went to was one of the first to offer a managed plan to smaller businesses with fewer than 50 employees. The numbers will work for most companies that pay over $100K in premiums.

The potential ‘catch’ to becoming self-insured

Because the right to self-insure is a federal law, you have the right to do it—however, states have the right to regulate insurance and some states have deliberately gone all in on the Affordable Care Act and have placed regulation barriers so small businesses can’t, for all practical purposes, take advantage of self-insurance. They have done this by imposing high dollar amounts that the companies must self-fund before they can re-insure at a stop loss. Other States have set limits as to the amount of people you have to insure.

Here is a list of the states that have no barriers to going with a managed self-insurance program like the one I described.

Alabama

Arizona

Georgia

Hawaii

Idaho

Illinois

Indiana

Iowa

Kentucky

Massachusetts

Michigan

Mississippi

Missouri

Montana

Nebraska

New Mexico

New York

North Dakota

Ohio

South Carolina

South Dakota

Virginia

West Virginia

Wisconsin

Wyoming

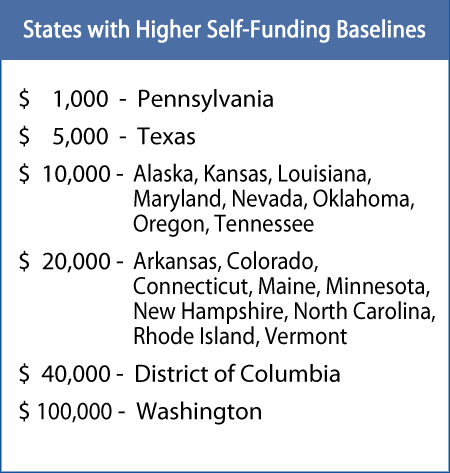

Some states mandate a higher self-funding baseline. As seen below, other than Pennsylvania and Texas, it becomes prohibitive for companies smaller than 50 people.

Other pertinent information I’ve found includes

- Florida requires over 50 people be insured

- Utah makes it difficult due to burdensome reporting requirements

- California just says no (what else did you expect?)

- And, New Jersey I do not have any information about.

Hope this helps. —dave